United States of Debt

Audio Recording by George Hahn

“I would like to come back as the bond market. You can intimidate everybody.”

— James Carville

America is blinking. The day after April Fool’s Day, President Trump “liberated” the United States from an eight-decade run as the world’s economic superpower, raising the cost of capital for the federal government, American companies, and consumers. If this sounds like stupidity, i.e., hurting others while also hurting yourself, trust your instincts. But don’t trust America. A blackout drunk is behind the wheel of the U.S. economy. All around us, horns (bear markets; consumer confidence plummeting to historic lows) are blaring. In the backseat is a cultist (GOP) who thinks the red lights Trump has blown through, and the accidents in his wake, are baller moves. Also in the backseat: a sulking teen (Democrats) who’s visibly upset but can’t articulate what they want or suggest a better route. Riding shotgun, though, is an adult the driver can’t ignore, the bond market.

(Dis)order

First-year economics students are taught that money evolved to make early barter systems practical. In his book Debt: The First 5,000 Years, anthropologist David Graeber argues that the barter story was likely a fiction created by Adam Smith; Graeber believes the earliest coins were actually tokens used to keep track of debt. “The moment one starts framing things in terms of debt, people will inevitably start asking who really owes what to whom?”

Debt is both a financial instrument and a social construct that binds people, firms, and nations to one another and links together the past, present, and future. As many anthropologists have pointed out, debt has moral implications around fairness, responsibility, and obligation, as it’s a tool through which we impose order. Historically, Judaism, Christianity, and Islam outlawed interest under most circumstances, counseled their followers against taking on debt, and advised debtors to repay loans promptly. When someone saves another person’s life, the person they rescued is said to be in their debt. When a criminal has served their sentence, they’re said to have repaid their debt to society. In a debt crisis, the real risk is not default, but a breakdown of the economic, social, and political orders.

How bad is this debt crisis? It’s too early to tell. But as former Treasury secretary Lawrence Summers explained, what has people most scared is the real-time erosion of the American-led economic order. Our reputation as a bastion of strength and stability, with our dollar and Treasuries representing safety, is in jeopardy. Increasingly, we resemble an emerging economy, where a crisis in confidence sends stocks, bonds, and currencies down and spikes interest rates. “If the United States isn’t credible, that makes the whole financial system less stable,” Summers said, adding, “we are more vulnerable to bad surprises from here than to good surprises.” One potential bad outcome? A stagflation cocktail of high interest rates, low growth, and high unemployment. This week, Fed Chair Jerome Powell warned that Trump’s trade policy and the resulting uncertainty may put us in a “challenging scenario” in which the Fed’s dual-mandate goals of maximum employment and stable prices are “in tension.” That’s Fed-speak for: This could be a clusterfuck.

Exorbitant Privilege

Since World War II, the U.S. dollar and U.S. Treasuries have been the backbone of the global economy. Charles de Gaulle called this “exorbitant privilege,” as it creates an asymmetrical financial system where foreign governments effectively subsidize American living standards and firms. Just how exorbitant is difficult to quantify, but, as economist Barry Eichengreen argued, the privilege isn’t what it was in the 1960s when de Gaulle complained that America was far too powerful. Still, our exorbitant privilege is a benefit, not a liability, as reliance on U.S. currency and debt lowers our cost of capital and increases the punching power of our economic sanctions. But in the wake of “Liberation Day,” analysts at Société Générale, Deutsche Bank, and Goldman Sachs expressed concern that America’s privilege is eroding.

Drunk on Debt

A financial adage frequently attributed to John Maynard Keynes, John Paul Getty, and others: “If you owe the bank $100 that’s your problem. If you owe the bank $100 million, that’s the bank’s problem.” This is the paradox of debt. The bigger the outstanding balance, the more the risk shifts from debtor to creditor … for a time, anyway. Trump, who bragged that he was “the king of debt” during the 2016 campaign, has leveraged this paradox his entire career, filing for bankruptcy six times. But compared to the federal government, Trump is a lightweight.

Bipartisan

Despite decades of warnings from economists and business leaders, increasing the debt is one of the longest-running bipartisan traditions in Congress. Conservatives (teetotalers) campaign as deficit hawks, then vote to increase the debt for unfunded tax cuts. Liberals (social drinkers) deprioritize debt by pairing big spending initiatives with modest proposals to increase revenue, i.e. taxes. And progressives (full-blown alcoholics) champion Modern Monetary Theory, which holds that governments with control over their own currency can finance spending without worrying about deficits or debt, as long as they manage inflation. How’s that working out?

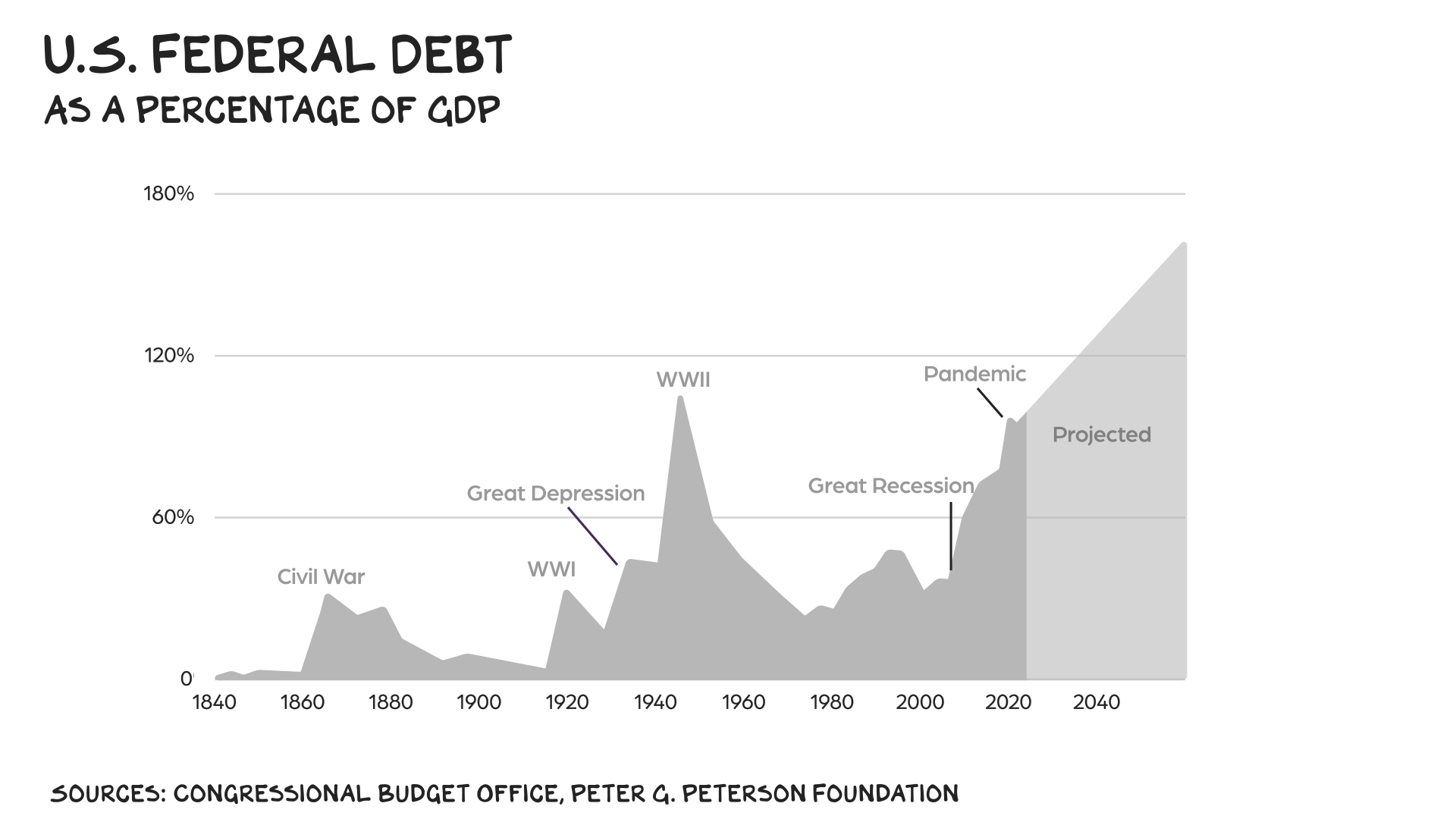

America is drunk on debt. We continue to drink at the bar long after last call. Spiking bond yields and the declining dollar are interventions. It’s not too late to get sober, however. I believe we should do it for our kids, as debt is a tax on future generations. But as I argued in my Ted Talk, despite saying we love our children, we’re waging war on them. There’s another reason to sober up: self-preservation. Sovereign debt crises have been the green mile of empires, from ancient Rome to the French monarchy to the Ottoman and British empires to the Soviet Union. America is exceptional in many ways, but we’re not exempt from history. Countries typically are not conquered, but go broke.

Vig

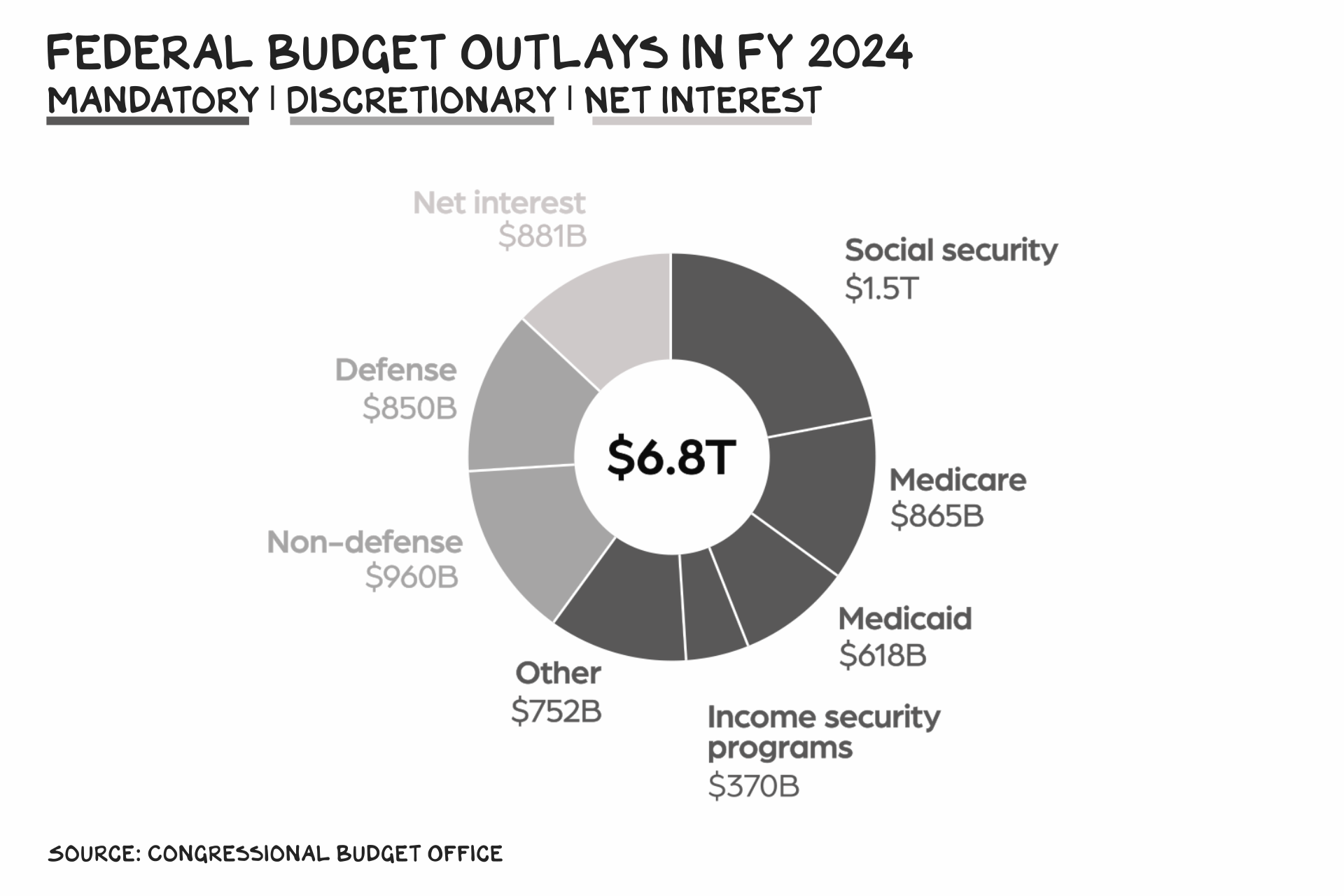

In budgetary terms, some people call the U.S. an insurance company with an army. This is correct insofar as our largest deliverables are the greatest military in history and a social safety net that lags behind those of other industrialized nations. But our fastest-growing spending priority is the interest on our debt. If current laws remain the same, net interest payments will total $13.8 trillion over the next decade, rising from an annual cost of $1.0 trillion in 2026 to $1.8 trillion in 2035, according to CBO projections. Rising interest rates increase the vig, crowding out mandatory and discretionary spending, as well as our capacity to respond to future crises.

Bonds Away

General Omar Bradley once said, “Amateurs talk strategy, professionals talk logistics.” His point was that war plans, even when the defense secretary doesn’t drunkenly share them with the Atlantic’s editor-in-chief on Signal, don’t count for much. It’s the unsexy stuff — supply lines, resources, and infrastructure — that wins wars. The world’s least-sexy financial instruments are U.S. Treasuries. They have historically been viewed as the safest bet in uncertain times. U.S. debt is both a shield that protects us from higher borrowing costs and a sword that, when used in conjunction with the dollar as the global reserve currency, guarantees American economic hegemony. But as with any weapon, if we lose control of it, our debt can be used against us.

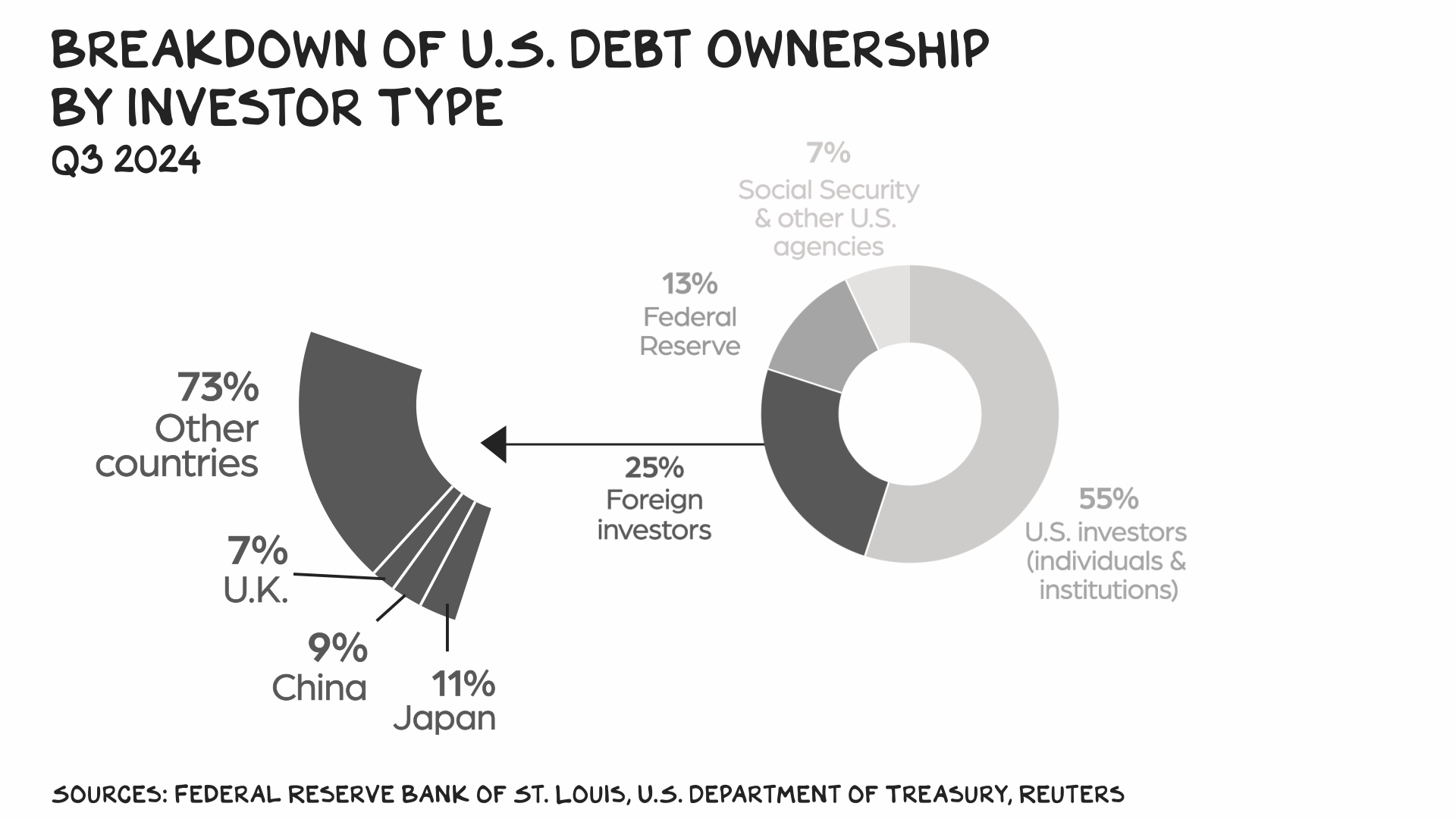

The U.S. debt is roughly $36 trillion. Nearly three-quarters of that debt is held by U.S. investors, the Fed, and various federal agencies, including the Social Security Administration; the rest is held by foreign investors. China is currently the second-largest foreign holder of Treasuries, behind Japan. After last week’s shit show, some analysts asked, without hard evidence, whether China was to blame for bond market volatility. That question misses the point. It’s not what China did or didn’t do, but rather what it’s capable of doing now that the Blinker-in-Chief has put a spotlight on our Achilles’ heel.

Dumping Treasuries raises U.S. borrowing costs, and, more important, undermines global trust in American leadership. It also hurts China, as a fire sale means they’ll take losses too, and a possible recession hurts everyone. Beijing’s fear of that economic pain has been a strong deterrent … until now. A trade war makes the pain real, meaning China has a lot less to lose (and potentially something to gain) by using our debt against us. And China has a pain-multiplier here: An increase of 50 basis points on a $36 trillion debt adds about $180 billion per year in additional interest — the equivalent of 13 aircraft carriers (we currently have 11), or $30 billion more than DOGE claims it’ll save taxpayers this year.

Game Theory

Our debt isn’t our only vulnerability. China holds $3.2 trillion U.S. dollars, more than any other foreign nation. Devaluing the U.S. dollar in the face of rising inflation would hurt Americans, as they’d pay even more for less. China’s mortgage-backed securities position is less clear, but as one of the top three foreign MBS holders it has the power to spook an already troubled housing market. China’s leading export partners are ASEAN (a 10-nation trading bloc in Southeast Asia) and the EU, followed by the U.S. Decoupling hurts both countries, but it hurts us more, as our exposure is greater and our pain tolerance lower. Remember, Americans freaked out about toilet paper and masks during Covid; China did actual lockdowns. We lost 36,000 service members fighting in Korea; before tapping out, China suffered 10x the casualties. We don’t have the tolerance for pain to exchange fire in an economic war with China. Ask Bowen Yang who’s more willing to endure hardship for the glory of their nation.

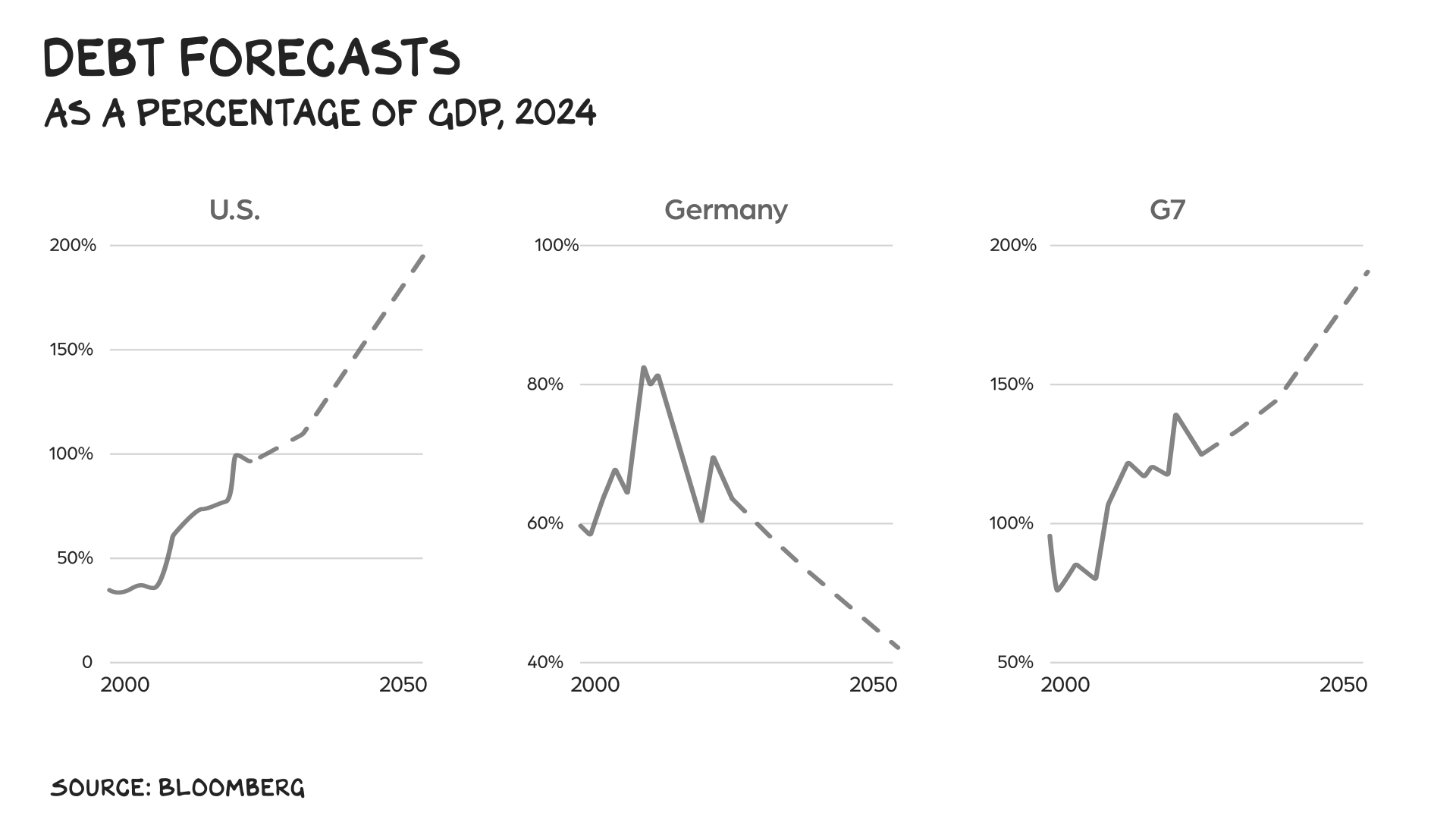

In Bund We Trust?

In the same week that U.S. Treasuries surged 50 basis points, yields on German bunds were largely unchanged. According to Bloomberg, that’s the biggest underperformance since 1989. In nonfinancial terms: As investors lost trust in the U.S., they found safety in Germany. One fixed income portfolio manager put it this way: “Bunds have been one of the only rate markets that has acted as a risk-off asset during recent volatility.” Are bunds the new T-bill? Too soon to tell. But if last week kicked off a debt crisis that unravels the world order, Germany — even allowing for a recent increase in defense spending — looks like a paragon of fiscal responsibility compared to other industrialized nations.

Lannisters

Ostensibly, HBO’s Game of Thrones was a show about knights, dragons, arctic zombies, and hot people. But underneath the veneer of sex and violence, the show was an epic story about the relationship between debt and power. As three economists who analyzed the political economy of Westeros wrote, “those who control the purse strings of the realm thereby acquire political power … [and] although it is a foreign institution, the Iron Bank becomes a key political player in Westeros.”

“Full faith and credit” is American for “a Lannister always pays his debts.” Instead of a mad king sitting on the Iron Throne, we have a very unstable genius (minus the genius) sitting behind the Resolute desk. His small council of sycophants know better, but, drunk on a cocktail of fear and greed, they cheer him on, claiming “He’s playing 4D chess.” This is the bullshit we hear from the Sparrows who can’t offer a counterargument to what is depressingly clear: The president’s actions are nuclear-grade stupidity.

Chess? At this point, the Western world is expecting him to eat the pieces. Trump’s game isn’t chess or checkers, but Russian roulette with bullets in five of the six chambers. The interpretive dancing and intellectual pretzeling of the remaining cultists doesn’t fool the Iron Bank, aka America’s creditors. In Season 1 of True Detective (#awesome), Matthew McConaughey needs something from his former partner, Woody Harrelson. McConaughey convinces him with a simple statement: “You have a debt,” calling on his sense of equity and a bond they share to reciprocate. Europe, China, the Middle East, and America all, at one time, imprisoned people who couldn’t pay their debts.

With 4% of the world’s population and 25% of global GDP, we have a debt to our allies, who’ve engaged in relationships that provide roughly 6x the prosperity relative to the rest of the world. However, that hasn’t been enough, and we’ve accrued unsustainable debt. From George Washington through George W. Bush, we borrowed $10t. During the first Trump administration, we borrowed $8t (Biden was $4t). We find ourselves ignorant of our debts and in a prison of our own making — a giant with feet of clay, ignorant to our vulnerabilities. In sum, we (America) are acting like assholes.

Life is so rich,

P.S. Prof G Markets has a weekly newsletter. Same No Mercy / No Malice approach, but focused on all things money. Subscribe here to receive it every Monday morning.

P.P.S. Section is launching a new AI for Programmers Mini-MBA. It’s built for developers by developers. Join the waitlist to get 40% off at launch.

I missed in the article ideas/ alternatives to bring debt to sustainable levels. Including maybe how to align incentives between democrats and republicans. Some sort of bi-partisan act on principles that survives presidential mandates? Also, we can always boast about US on aggregate doing better than the rest of the world but this misses some forgotten or understandibly unsatisfied segment of the country, ie the MAGA base. When can we have an article that tries to emphasize with that base and propose alternative solutions to their problems that the ones Trump is proposing?

Sorry the MAGA reference is a mistake here. I meant to refer to some segments of the population where all these globalization benefits have been less aparent for them (ie some industrial cities/ regions etc) that in the recent election have looked for the Trump and MAGA platform for change

Excellent show. Thank you Prof G! I would love to know how to push Congress to act but we have a cult in Congress right now. Still, I have a list of people I will write.

This piece is full of dramatic metaphors but short on economic reality. The U.S. government is the issuer of its own currency — it can no more “run out of money” than a stadium can run out of points. Treasury securities are not a credit card bill; they are interest-bearing assets held by the private sector. Interest payments on the debt are income, not a looming crisis.

The idea that rising interest costs will “crowd out” other spending only applies to households. The federal government doesn’t need to “find” money to spend. Its only real constraint is inflation, not solvency. And interest rates? They’re a policy choice. The Fed can set them wherever it wants.

Fears that China could weaponize U.S. debt are also overblown. If China sells Treasuries, it gets U.S. dollars in return — it’s just switching accounts. The U.S. government’s ability to spend remains unchanged.

And the comparison to Weimar Germany? That inflation was driven by reparations in foreign currency, not domestic policy excess. It’s not remotely applicable to a country that issues its own free-floating currency and doesn’t owe debts in foreign denominations.

Let’s stop pretending that federal finance is like a household budget. It isn’t. Deficits aren’t inherently good or bad — they must be judged by real outcomes like employment and price stability, not scary analogies or rising debt figures in isolation.

I don’t think the 50bps calc is right as it assumes the US gov pays a floating rate on its debt. The rise in rates only impacts that debt that has to be rolled over at the higher rate. The old stuff all pays the fixed coupon at the time. Call me for a job.

you aren’t intellectually honest if you completely ignoring what has to be done. you can argue how bad its being done but there is no question that there is a merit to the goal.

Would love to get your thoughts on the Treasury, as I don’t think the Gov’t controls all the levers in play when it comes to debt.

Didn’t Deutsch Bank sell Trump’s personal debt to Russia before T ran the first time? Isn’t that part of the Debt that controls T’s actions? And in part, our Country?

Not a word about gold…

As I understand it, the US Treasury has burned through all the cash in its checking account and done other actions to deal with the debt ceiling problem. Assuming it is resolved sometime this spring or summer, the Treasury will need to refill is checking account and deal with a number of accrued but unpaid items. So there will likely be another TRILLION of debt added in the next six to nine months. I am not sure what such a dump of Treasury debt will do to interest rates. Stay tuned!

Great article; well reasoned and based on widely accepted facts, as usual. Only one quibble, US share of world GDP using the widely accepted purchasing power parity instead of current exchange methodology is only 15.5%. Most Americans are reluctant to use this methodology because we are obsessed with being #1. China’s GDP exceeds that of the U.S. by at least 25% although their per capita GDP and standard of living are significantly below ours.

CHINA hugely exaggerates their GDP numbers. Estimated by 25%.

Wait what? You actually think the US government wants to balance its books? Bro we have fiat currency. The entire system is predicated on racking up debt that cannot be repaid. That is fractional reserve banking and lending and borrowing. It’s paper money. It’s fake. It works to increase productivity. Inflation is a silent tax that keeps people pushing to deploy capital better and better. Come on Scott, I know you know this. Don’t fall victim to the thinking of “why don’t we balance our budget”. It cannot be balanced by design. We crave growth over sound money.

Provocative. And brilliant. 100% to the point. Let’s wait for the economic laws of gravity to prevail.

Excellent as usual

Did you miss the last 4 years of MMT? I guess the other team was on course to fix everything?

Great essay. I usually complain about something. Nope… this is near perfect and oh so important. KUDOS!

No matter what you hear, no matter what you read, you can be sure that whatever is going on in the economy is not good for people like professor Galloway, who has the responsibility to manage four or five houses, pay a small cadre of private employees (may or may not be citizens), and convince people that he’s “got their back.”

Thank you Paul !! On spot !!

Wonder what will happen to Treasury rates if Trump sacks Powell and inserts a more malleable Fed Chair who is willing to cut short-term rates in the face of rising (tariff and weak $ fueled) inflation. My hunch is that the marginal buyer of US Treasuries will require a higher rate.

According to Reuters, U.S. bond giant PIMCO (i.e. the smart guys at the table) recently recommended dialing down (i.e selling) exposure to the U.S. dollar and long-dated Treasury bonds due to protectionism in US trade policy.

Have a great weekend Scott (Bessent)….

One thing about debt – it can be restructured. For instance, China is our a communist, totalitarian regime, with now respect for Western Culture, law or morals. See their treatment of Uighurs, trampling states rights and violating international law in the South Pacific, theft of Izp, invasion of Tibet, where do i stop. So if they are our enemy, at what point do we invalidate our debt. do we wait until a shooting war over Taiwan or maybe just another close encounter with one of their ships or planes? We don’t have to default, maybe just offer to buy back our debt at 10 cents on the dollar. They could always make a better deal with another sovereign fund. And since the bond market can be easily manipulated by a bad actor, maybe its not the adult in the passenger seat. If you really think there will be a calamitous trade war, recession and bear market over tariffs, i got a bridge in Brooklyn to sell you. Countries will come to the table so as not to lose access to the US market. Israel, Argentina, Italy, Japan already talking, India would love to supplant their regional adversary. How about reducing interest we pay the CCP and increase the rate we pay to friendly non-tariff countries. Just saying, let’s let it play out before you go all humpty-dumpty.

Don’t always agree with Prog G’s politics…but first paragraph of this article is brilliant. The rest is pretty damn good too.

Scott, THANK YOU

Very clear explanation. Listening to NYT interviewing Trump voters in Michigan, they attributed the loss of jobs to trade and Trump was the only one who could fix it. Are there any RED Lines that if crossed would indicate that we went to being potentially (high Risk) to it happened (the risk occurred)?

Your “United States of Debt” article raises valid concerns, but I must challenge several points. Trump isn’t a “blackout drunk” driver—he’s the first recent president to confront debt head-on, inheriting a crisis after $10 trillion borrowed from Washington to Bush. His $8 trillion added reflects a bold pivot to reduce foreign dependency, not recklessness.

You overstate China’s leverage with its $3.2 trillion in U.S. dollars and Treasuries. China has lost $3 trillion in 18 months, facing ghost cities, unemployment, and a potential CCP collapse by 2040. Their population is four times ours, so surpassing U.S. GDP isn’t surprising—but a Taiwan invasion is the real risk, not our debt.

The U.S. can recover by adopting household strategies: manage debt, reindustrialize, cut non-essentials, and innovate relentlessly. Rising interest payments ($1.8 trillion by 2035) are concerning, but America’s resilience and innovation can overcome this—not historical collapse narratives. Let go of your woke ideologies Scott, you know better (especially for a dude worth $200M)

So how does the average American, who has been kicked down at every turn, ( tech bubble, housing bubble , covid crash, out of control inflation-housing,-food- energy- healthcare) try to keep his head above water?

I have what appears to be a good paying job, with good benefits, retirement options, COLA’s,ect. Yet every year I fall further and further behind, and retirement becomes more and more distance.

Congress members only care about getting reelected, and their corp. donors.

Stop whining. The Chinese save 40% of their income, you can at least manage 10%.

Scott, First, I am a big fan, and really used to love reading your stuff. More and more it is so pre-loaded with pejorative partisan politics that it is honestly tough to read. Yes, I believe your facts are probably tight (I only trust statistics that I have manipulated myself), but the coefficient of blame is tiresome and honestly you are above that level of mudslinging. Most of us are here to hear your nuggets of wisdom (of which there are many), not to be lectured on politics which we already must suffer through 24/7 during our normal duty day. IMO, your weekly column is Adrift from what used to anchor your readers appetite. Just my .000000024 BTC. Keep up the good work.

Please run for office Scott

Inflation reduces debt in real terms and increases the nominal price of everything.

Always very interesting but, as a non English native speaking like me ( I am Italian), quite frequently your “lingo” is quite difficult to understand since you relate of past night tv show or other US cultural things which are difficult to know for also an international audience like you have. I understand straight language is also your personal stamp, but to go a bit easier on that will help us ( foreigners ) go get the message. Thanks

Well sad Scott. We are going down a dark, one way street. Shame to those that drink the lemonade for ego and power. Failure and loss relationships are the new reality to come. We need help.

You grossly overstate the impact of China. Let’s consider:

1. UST (bonds, bills, notes) outstanding is $27.2T.

2. Foreign gov’ts hold $8T UST.

3. China holds $0.75T UST.

4. Daily UST trading volume is $1.05T.

5. China holds less than 10% of all foreign UST holdings.

6. China holds 2.3% of UST.

7. China holds less than a single day of UST daily volume.

8. China holds $3T USD to underpin the yuan – USD peg.

9. China requires massive amounts of USD daily to settle its energy import account.

10. Interest rates impact daily UST trading, but are irrelevant to the US until it auctions off new batches of UST – refunding.

Whilst the US needs to attend to its own accounts, China exerts nearly zero influence on the UST market other than the ill-advised writings of journalists w an agenda.

It will be fine.

JLM

Trump hasn’t even articulated a consistent goal of the tariffs. Are they a long-term play to re-shore manufacturing? If so then why is he so eager to make “deals” in which tariffs are negotiated away in the short term (not that he’s had much success with that approach either)? If he’s so keen to revive American manufacturing and support the working class, then why is he destabilizing the dollar, canceling offshore wind construction permits mid-project, and telling Congress to repeal the CHIPS Act — all moves that make it harder to generate manufacturing investment and that threaten working class jobs? If he’s trying to weaken China then why is he tariffing all our allies who otherwise would probably join us in countering China’s economic shenanigans (and whose support we could leverage)? Why are we tariffing shoes and apparel — does the White House seriously believe that Americans want to work long hours sewing underwear in factories when they could be making more money, say, in the trades? The entire trade policy emanating from Washington is like dumping raw sewage into our economy’s drinking water supply. It is an act of self-poison.

onshoring of strategic manufacturing such as pharmaceuticals, electronics, chips, specialty metals, etc. COVID showed what happens when you are dependent upon an enemy for strategic material. Biden couldn’t even utter “Chinese virus” he was so compromised. And polls show there are many Americans who would love a good stable manufacturing job, Henry Ford had it right, build a car that your workers want and pay them enough to buy it.

MMT gets some things wrong; but its not all alcoholic delusions. I’ll make two points: 1) the 13% of the debt held by the Federal Reserve is literally what our right pocket owes to the left pocket. When that is paid back to the FED it returns to the Treasury. Call it currency manipulation or inflation of the money supply, but it’s not the same as bonds held by China. And 2) What is the appropriate cap rate for the United States of America? If the USA was an income producing property, an investor or lender would look at debt this way: $27 tn in annual GDP at a cost of $7 tn per year in federal government spending. That’s a NOI of $20 tn per year. At a 5% cap rate that’s an implied value of $400 tn and a current LTV of 9%. (I know this is overly simplified, but it makes the point)

Over a trillion a year in debt service is too high and I agree it is worrisome. But a United States economy that does nearly $30 tn a year in goods and services is the richest in the history of the world and there are some big tasks ahead that will be worth borrowing money for. We need not be afraid of it. Personally, I’m more worried about an executive branch that treats equal protection of the law as a technicality to be ignored

The left may be waking up. Start by acknowledge the corruption of fake NGOs under USAID umbrella. Or that the massive Biden ‘Infrastructure’ bill was just a scam payback to Unions. Just be sure that Trump is front and center, and not Obama or Biden. While military waste was a constant in the left media, few acknowledge that the ‘Great Society’ spending was larger. At least we did not have WW III with defense spending. Social spending gave us $1.2T student debt load, BLM, and Harvard grads who think there are 12 genders. Detox for US is to stop being the world’s policeman, and have equal trade agreements. And for wokes to get real jobs, not just hide in Academia or under the protection of a fake NGO. Taxpayers do not want to fund your idea to pay for ‘feminist writing programs in Bolivia’.

Agreeing more with you than you do with yourself. Bravo and well played.

JLM

I didn’t realize they’d invented a chatbot trained on Jesse Watters’s drunk tweets. But here we are.

What’s the end game here? On the surface, it looks like pure pettiness with the intent to bring all to their knees by making brash moves and then playing stupid or reversing course when there are repercussions. Even if liberals have no answer or coherent alternative, this is going to lose the next set of elections. So are they just waiting for the burning of the Reichstag? Otherwise, I don’t get it.

Interesting points, but nothing with respect to China’s need to keep the Yuan pegged to the US dollar to maintain their currency/economic stability. They do that with the $3T in reserves they hold, so that isn’t quite the threat one thinks. Further, how much and for how long can they manipulate the bond market when they only hold around $700B? In short, they have cards certainly because they aren’t idiots, but i think their hand is materially exaggerated here.

If our trade with China collapses — which may well happen if this tariff stand-off isn’t resolved — then China has far less incentive to hold our debt and peg its currency to the dollar. It might want to hold dollars for other reasons, but a major purpose of holding our bonds is to keep its exports to America cheap. Once that reason is gone, China might feel freer to dump bonds.

“-a giant with feet of clay, ignorant to our vulnerabilities” . . . or perhaps, more apropos, Wile E. Coyote (Genius) and his ACME Glue. As I have been saying since 2015: “Trump (and Sanders for that matter) are brining up several subjects which need discussion and dealing with (trade, immigration, proxy wars etc.) but he hasn’t got a clue how to actually deal with these issues”

Great stuff Professor Scott.

In the ring, China is prime George Foreman and Trump is Ric Flair. We will need diplomacy and integrity to crawl out of this disaster. So much irony; the far left used to foment protectionism and crackpot economics like MMT (and never foreign trade pacts); now the MAGA cult owns it along with all their conspiracy theories and related bigotry.

The enormous U.S. debt is the predictable result of something called the Trillin Dilemma, which was correctly identified by economist Robert Trillin in the 1960s. It basically states that when a currency becomes the global reserve currency, that becomes the main export, hence you are signing up for huge debt. Your domestic economy will be destroyed except for 2 things: a financial industry (which profits from the export of dollars, in the case of the U.S. ) and a huge military (to support the reserve currency status). Sound familiar?

This is why China has no interest in becoming the global reserve currency, and takes active steps not to let that happen.

Scott, I am in Europe now (Germany, France) . Except for electronics, things here are manufactured by the EU countries. I have literally looked at the cups, hairdryers, etc. in my hotel room… and none of them say “Made in China (or Vietnam).” I fear what will happen to their society if they allow China to swamp them with consumer goods.

So—perhaps the dollar being the global reserve currency and the gutting of our domestic manufacturing economy that has been the result has led us to Trump? Was it worth it?

Elizabeth, you think your stuff is made in Europe, but it is pre-made in China and assembled at the last minute in Europe to meet the EU’s “local labor content” regulation.

Corker today, Prof! Thx for all the data, well packaged.

I enjoy reading your newsletters even though they scare the shit out of me. Do you think he’s doing this partly to elevate Crypto, enrich himself and his buddies and then to eventually overtake the dollar/gold?

Dude, don’t let your TDS distract from your insights. I’d like a graph that not only shows who holds our debt but who is on the hook to pay for it. Spoiler Alert: the American taxpayer.

How does your snipe relate to this post? You “taxpayers” keep sponsoring and electing people who expand the very hole you say you despise. So, who here has a mental problem?

Thanks for engaging Michael. I do not consider it a snipe. I have respected Scott for his insights and direct expression for years. He is unafraid to criticize any institution or industry including his own. My point is that his rhetoric may turn others away and they would miss his more specific point. Why do that? Since you have not included yourself as a taxpayer, what qualifies your exemption?

Nice summary!

This was a great Dmv read. Thanks for compiling this for us Scott