MeWork

Two years ago, WeWork’s IPO was aborted, and the company was put on SoftBank life-support. Things changed yesterday. WeWork took its first steps in the public markets, opening at $9.5 billion, which is a fifth of its 2019 valuation. Sanity restored.

The stock’s doing well. It closed up 13.5%, which is an especially nice gift to Adam Neumann, whose 11% ownership is now worth more than $1 billion. He celebrated in standard douchebaggery: spraying champagne at the Standard Hotel in a shirt that read “Student for Life.” It took the greatest catastrophe in IPO history for Neumann to realize he’s not fit to teach.

But don’t let the stock price fool you. WeWork still loves burning money. The company lost more than $6 billion over the past 18 months, a nasty habit investors expect it’ll drop once the world returns to more flexible working patterns. I wrote about this habit earlier this year — not much has changed.

[The following was originally published on May 28, 2021.]

MeWork

I’ve lost a lot of other people’s money. The most stressful times in my life have been when people believed in me and invested tens (if not hundreds) of millions in my company or idea, only to see their capital go up in smoke. I’ve also made a lot of people a lot of money — but only in America would someone with my (lack of) pedigree be given this many swings at the plate.

To be a truly great investor or operator/CEO, you need to be a bit of a sociopath: You have to be able to sleep at night even as you lose other people’s hard-earned money or lay people off. Working with “OPM” (i.e., Other People’s Money) is often phrased as a positive, but the real luxury is to be in a position to lose your own capital. If things go wrong, it’s a private failure.

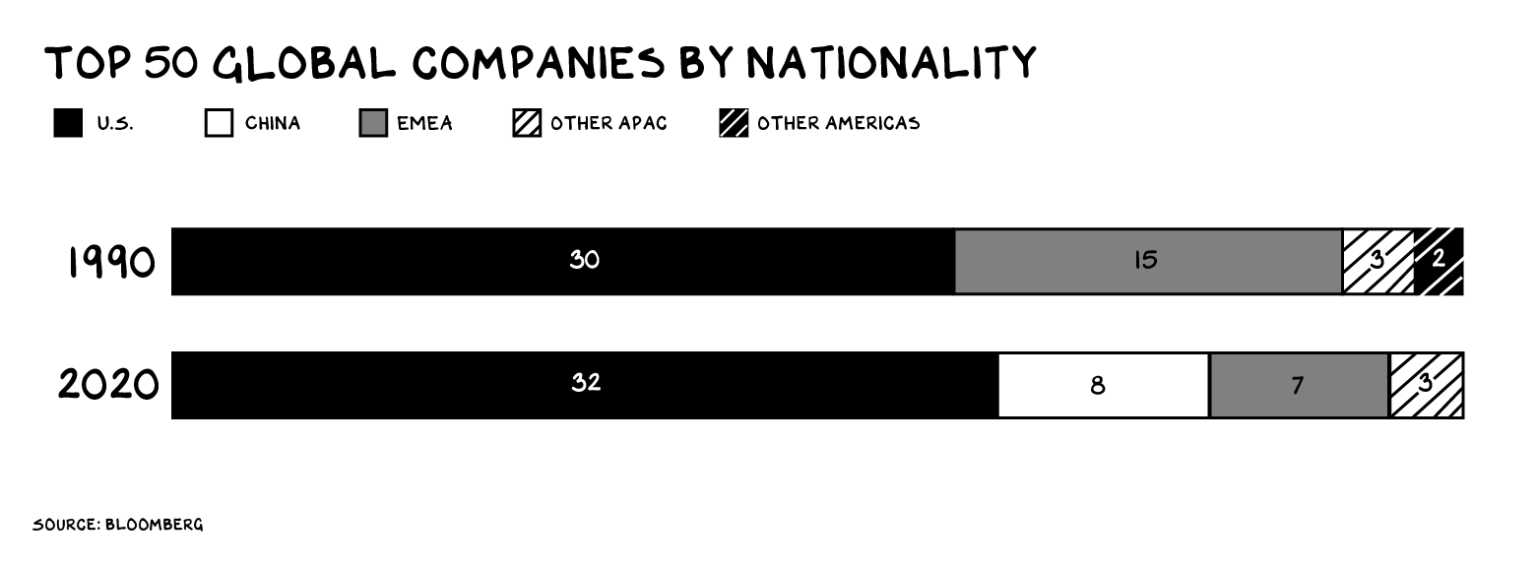

The willingness to risk capital on a captain and harpoons (the 19th century whaling sector was proto-venture capital) has always been a key ingredient in the secret sauce of the U.S. economy. But the secret is out. While the U.S. still produces the most unicorns, and the most mega-corporations, China is gaining … fast. Interestingly, despite the rhetoric, re: China challenging U.S. hegemony, it’s European innovation that has drowned in the rising red tide. But that’s another post.

We should celebrate billion-dollar successes, so long as they come at the risk of failure — the whaling captain and the entrepreneur earn their wealth in part thanks to their willingness to come home empty-handed, or not at all. However, there’s a new class of billionaire in America. Meet the MeWork generation, which makes their fortune despite returning to harbor with less than they embarked with.

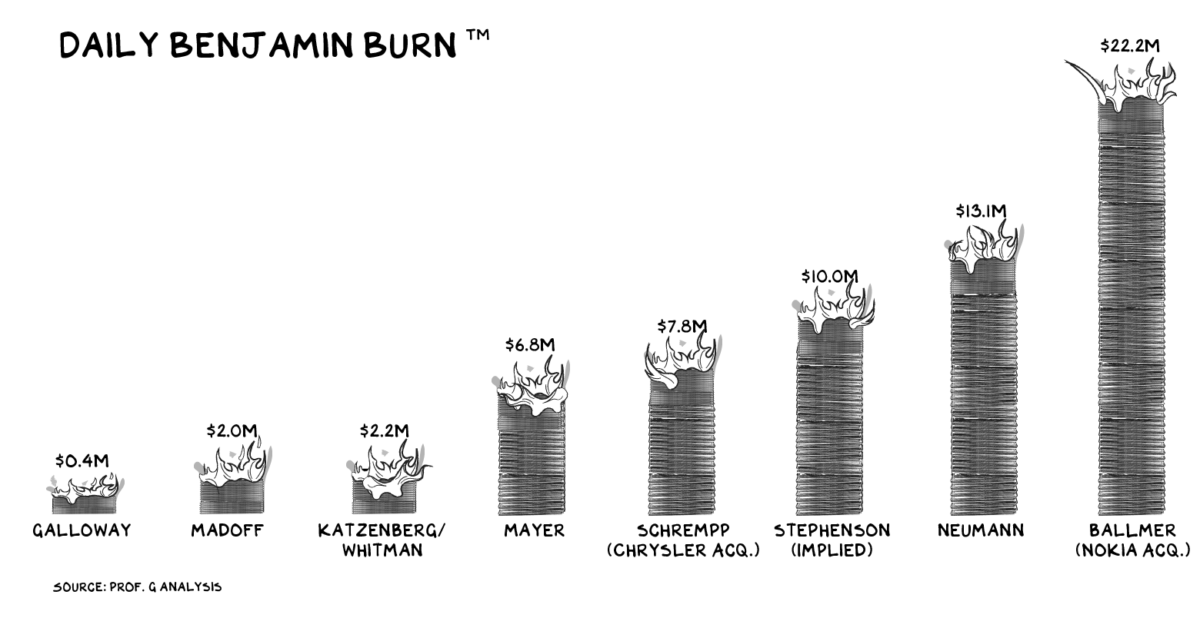

To help identify members of the MeWork generation (they can be any age), we’ve devised two metrics: the Daily Benjamin Burn™ (DBB) and the Earn-to-Burn Ratio™ (EBR). The first is how much money an executive lit on fire per day during their tenure. The second is the percentage of those lost Benjamins they siphoned off for themselves — think of it as a commission on destruction. In an efficient and fair (dangerous word) market, the EBR ratio would be zero. If we can measure someone’s burn in daily stacks of hundred-dollar bills, they’ve created no value and should get no compensation. Spoiler: That’s not what happens.

Daily Benjamin Burn™

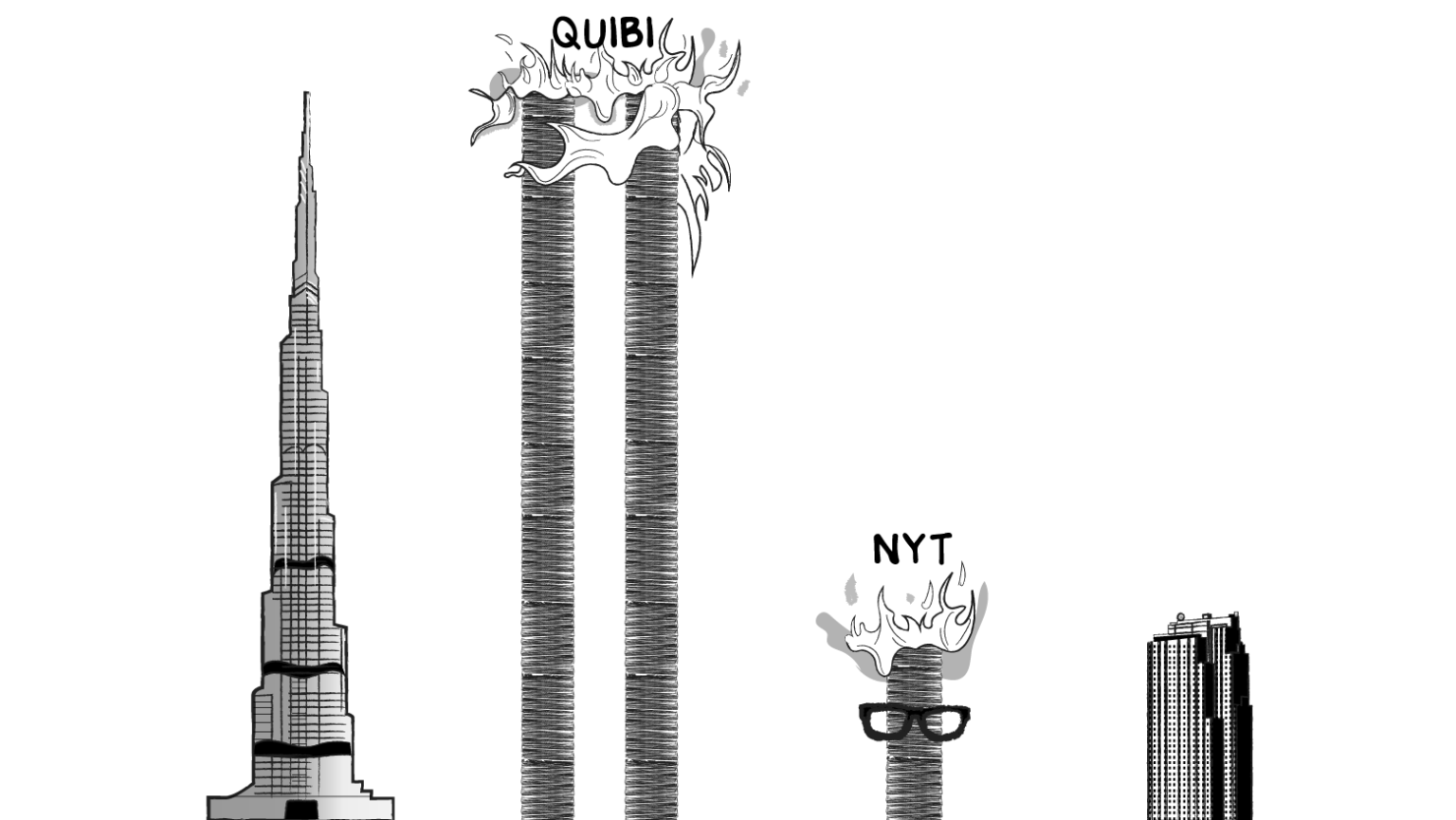

What does the DBB look like in practice? A lot like Quibi. That likely won’t mean anything to you, unless you’re one of the dozens and dozens of people who subscribed to the short-lived short-video service. In 2018 Jeffrey Katzenberg and Meg Whitman raised $1.75 billion, launched a bad app with worse content, and shut it down six months later. Roku combed through the rubble and found $100 million, so Jeff and Meg immolated $1.65 billion in 750 days, or $2.2 million per day. If you stacked that $1.65 billion in 100-dollar bills, you’d have a pile over a mile high, or the height of 2.2 Burj Khalifas, the world’s tallest building.

Eating My Own Benjamins

In 2008, I raised $600 million from a hedge fund, became the largest shareholder in the New York Times Co., and ran an activist campaign against the Gray Lady. They put me on the board, where I ranted about the evils of Google, advocated for the divestiture of noncore assets, envisioned sunlit uplands of subscription revenue, and … lit Benjamins on fire. During my 24-month tour of duty watching the Great Recession kick ad-supported media in the groin, I managed to turn $600 million into $350 million, for a DBB of about $350,000. The stack of Benjamins I lost would have reached only to the top of 30 Rockefeller Plaza. Only. Jesus …

I. Want. To. Throw. Up.

Earn-to-Burn Ratio™

Jeff, Meg, and I all made an old-school mistake. We failed to find a greater fool (e.g., the public markets, gullible board members, SoftBank) to secure a mega-payout for our Bonfires of the Benjamins. I was paid approximately $500,000 in board fees and a retainer from the fund; I speculate that Jeff and Meg pocketed more (their compensation remains private). But none of us pocketed millions.

That brings us to the Earn-to-Burn Ratio™ and the Hall of Fame for broken compensation.

EBR Hall of Fame

In 2012, Yahoo replaced its CEO with an executive from Google: Marissa Mayer. But the new chief executive made a series of poor decisions, including canceling the company’s telecommuting policy while she worked from home herself and paying $1.1 billion for a porn site, Tumblr. (Note: Six years later, Yahoo sold Tumblr for $3 million.)

When Mayer took over, Yahoo was valued at $14.4 billion (not including a 20% ownership stake in Alibaba). In July 2016 the company sold itself to Verizon for $4.5 billion, and Mayer was gone. That’s $9.9 billion turned to ash in four years (or 13.5 Burj Khalifas), for a DBB of $6.8 million. Mayer’s compensation began with a $30 million signing bonus and went up from there, totaling an estimated $365 million, giving her a $250,000-per-day commission for destroying $7 million per day of other people’s money. That’s an EBR of 3.7%. Shocking, sure, but not the gold standard.

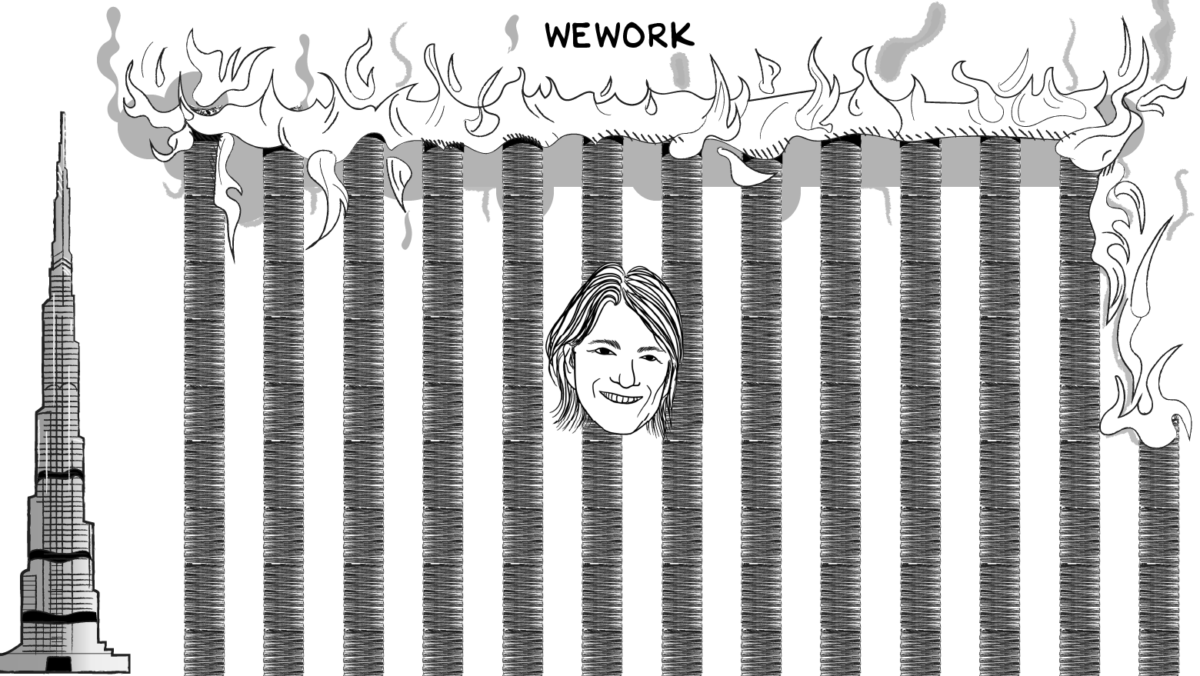

Adam Neumann founded WeWork in 2010, but he didn’t start burning Benjamins at epic scale until SoftBank began shoveling billions into the WeWork furnace in August 2017. By the time Neumann was fired in September 2019, SoftBank had invested $10.3 billion; a few months later it wrote off $9.2 billion of that. That’s a $13.1 million DBB on SoftBank’s money alone, or like flying a decade-old Gulfstream 450 (I browse planes at night — pathetic) into a mountain … every day. Impressive, but only half the story. Neumann’s compensation for this value destruction was complicated by his ouster and a subsequent lawsuit, but we estimate he made off with around $1.023 billion, most of it coming out of SoftBank’s deep pockets. That’s $1.5 million per day during those two years: an EBR of 11.1%.

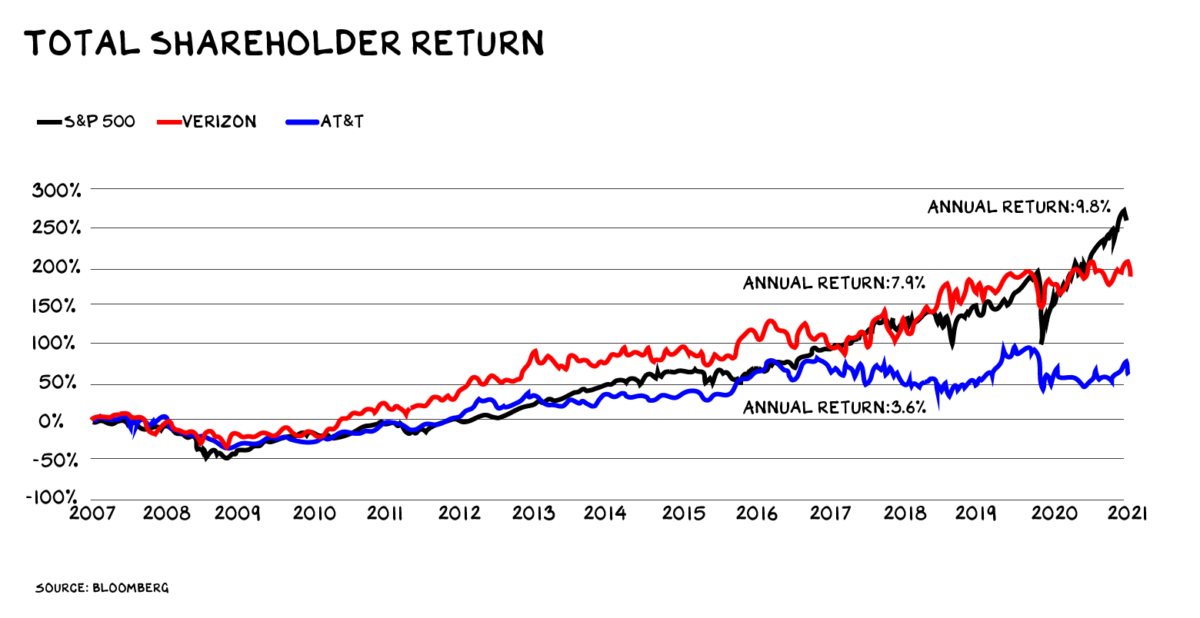

Joining Mayer and Neumann on the podium is Randall Stephenson, who ran AT&T from 2007 to 2020, when his chief lieutenant, John Stankey, took over. If you owned AT&T stock in 2007, you’ve collected $25 in dividends since, but you’ve also watched the share price drop from $39 to $29, for an aggregate annual return of 2.5%. This was a period when S&P 500 companies as a whole returned 9.8% a year — much of it on the back of AT&T’s own mobile and data networks — and AT&T’s competitor Verizon returned 7.9% to its shareholders. How did Stephenson manage this? Among other mistakes, AT&T spent $67 billion to buy DirecTV (a pending massive write-off whenever Stankey needs a distraction from some other screw-up), blew $4 billion when it failed to acquire T-Mobile, and spent an additional $108 billion to buy WarnerMedia, which Stankey just sold to Discovery. To his (partial) credit, Stankey may have managed to net the Warner deal out as a wash.

So while Stephenson didn’t destroy capital outright, he was a poor steward. Had AT&T eked out even a 4% return from 2007 to today, it would have made an additional $50 billion for shareholders. That’s an implied DBB of $10 million. How did the board respond to Stephenson’s 13-year-long sideways run at the iconic firm? His total comp was at least $250 million, including a $64 million pension as a parting gift. That’s an EBR of “only” 0.5% but still a huge payout in the face of mediocre performance.

Honorable Mention

In April 2014, toward the end of Steve Ballmer’s controversial run as CEO, Microsoft closed the $7.2 billion purchase of 1999’s leading mobile handset maker, Nokia. Just 15 months later, Ballmer was gone, and the company wrote off $10 billion for the failed acquisition — the deal was so bad it ended up costing Microsoft more than it paid, mostly due to severance for laid-off Nokia employees. That’s an incredible $22.2 million per day, the highest DBB we could find. (Ballmer only made $1.65 million his last year at the company, so a minimal EBR.)

Burning Benjamins doesn’t just happen in the U.S. In 1998, Daimler-Benz acquired Chrysler for $35 billion in the largest industrial merger ever at the time. After nine years of culture clash and billions in losses, Daimler unloaded 80% of Chrysler to a private equity firm for $7.4 billion, valuing the company at $9.25 billion. That equates to an impressive $7.8 million DBB.

How do these corporate money losers compare to the largest and longest-running Ponzi scheme in history? Bernie Madoff ran his fake fund for nearly 30 years, costing investors an estimated $19 billion. The date his fraud began is disputed, but assuming it was 1980, that’s a DBB of just under $2 million per day. A massive, decadelong legal project has repaid most of these losses through fines and settlements, and Madoff died in prison, but only after a multidecade run paid for by the destruction of thousands of people’s economic security.

MeWork

Growing up, I loved to watch my dad pack for business trips. He smelled of Aqua Velva and draped his Izod sweaters over a Ram Golf bag. He’d iron the mammoth collar of his Pierre Cardin shirts, fold them around a piece of wax paper, and lay them into his Hartmann luggage like newborns. It was ceremonial, just as when he would wear his kilt. Elegant yet masculine. During one of these pre-business-trip ceremonies, when I was about 8, my mom walked in. I looked at my dad’s stuff and asked, “How come dad is so rich, and we’re so poor?”

My dad loves this story and laughs out loud when he tells it. But it wasn’t funny. He’s been married — and divorced — four times. There was some financial stress, there was incompatibility. But the real fissure was that there were two Americas … under one roof.

Whether we’re executives, parents, or just average citizens, we need to ask ourselves: Have our interests diverged from the people who matter most to us and society? Do our spouses, children, neighbors, employees, and countrymen win and lose in reasonable harmony? Are we part of a family, part of a nation? Or have we become the MeWork generation?

Life is so rich,

P.S. The world’s biggest tech companies are constantly running experiments. The key to keeping up is innovating, not replicating. Section4’s Product Experimentation Sprint will teach you how. Registration closes next Thursday. Join us.

Great piece. And to the person griping about inflation, where have you been for the past 30 years? Why do u think college enrollment is dropping? Why do you think rents are insane and homeownership is out of reach for so many? What do you call it when assets trend skyward while wages stagnate? Why do think there’s so much health bill related bankruptcy? Inflation’s been there, it’s just not reflected in the headlines.

I loved every bit of it. Other than your new “Metrics” that you coined here, I thought there are lessons about acquisitions gone wrong as well. Have you written about acquisitions gone wrong or would you be writing about it?

Thanks as always

Your writing just keeps getting better and better.

Instead of actually delivering a tangible product or services lot of new startups are focused on getting mighty valuation. This is followed by exit in future and finding a new green field. They become a talked about brand and a tribe of which lot of big investors want to be part.

A world in which people lose billions of dollars while getting richer is not capitalism. It’s broken capitalism.

Probably the best write-up in the world of finance that I’ve read over that past 5 years. Rock-star performance

Great write-up! CEOs’ remuneration packages should be a combination of multiple elements rather than these crazy compensation packages, i.e. should include performance/success rate during and after the tenure, add some skin in the game. Also, it’s crazy how come all those investors/venture capital firms with their “expertise and mastery” can’t see through some of these BS artists, a.k.a “founders”.

What would Steve Ballmer’s rating be in a National poll? My bet is that it would be higher than he deserves

Very interesting concept and perspective, thanks for bringing this so straight and fact based. No doubt we live a Me work moment where the me is becoming much stronger than the we. 2 perspectives which I would love to hear your perspective and thoughts in a future article:

– how in a “ me work” environment we will be able to succeed confronting such challenges we have as society ( environment, poverty … all the 17 SDG )

– on EBR : we can personify the concept into one person as your examples, but seems to me there is an industry behind it; bank advisors , head hunters, consultants many benefiting from this EBR but cynically hiding theirselves behind such pronounced failures.

I think AOL / Time Warner merger could have the biggest DBB of all time.

The central point of this wonderful article (to me, anyway) is how key executives can burn so much shareholder value and be rewarded on the way out. And this must be because remuneration boards are in on the scam. At some point there will have to be shareholder activism insisting on “we are all in this together” deals that do not reward failure. And those deals should also specify a minimum expected growth to ensure those executives take chances above and beyond letting the ship cruise on. Activist shareholders have slowly forced changes to other aspects of management (climate awareness in oil companies for example), so this is possible. Unlikely, but possible? Scott, lead on.

Enlightening and depressing all at the same time. The key to stopping bad business is more voices like this. Thank you.

Great article, Scott. Absolutely loved it. Admittedly not a big fan of a lot of your pieces but this one was exceptional. Chapeau bas….

I started out in the 1980s with a “winner take all” mentality and lost that business. It cost not just our family but others as well. I am now the owner of a small (fewer than 10 employees) business started in 1993 and solid. Sometimes I feel inferior as a leader when I listen to your podcasts or read the newsletter because I get confused about what success is. Then I remember that I value the company that we created because it takes care of all of us from our vendors down. I am empowered to align my values with my livelihood. I know I could have taken more but I have done my best without regret. That’s freedom.

I can’t help but laugh as I read this…I guess I should be crying but I don’t know why I always laugh when something makes me nervous. By the way, who does your illustrations?

Am not sure what I would be joining !!!Clarification please !!!!

Every human loves a false idol its what keeps us from being robots.

You wound me up with the EBR and DBB…then you literally brought it home with the story about your dad…I can relate to 8 year old professor G.

Not sure why I feel this way about Adam/WeWork but I do – it so very much felt like the Emperor’s New Clothes to me – how in the hell did people not just say, “you’re a realtor!” And after listening to him for two minutes how did investors not see this?? How are investors to f*n gullible? I wouldn’t buy a stick of gum from him..

RE: Your dad, my dad: Sometimes the “salesman” in all of us has to “spend a little” to look the part.